The EU has set itself renewable energy targets up to 2030 to meet its climate-change ambitions and, more recently, to increase its energy security, in light of the Russian invasion of Ukraine. Achieving these renewable targets will require a step change in the installation of new solar and wind capacity. How realistic is that? There are plenty of obstacles in the way that will make it difficult to achieve these targets, including rapidly rising material and financing costs; structural labour shortages, policy uncertainty and an unwieldy planning and permitting system acting as a brake on the rollout of major infrastructure projects. Even with the best of intentions, policymakers will find it difficult to achieve their renewable targets by the end of the decade.

The EU wants to expand renewable energy to address climate change and reduce reliance on imported energy

The European Union (EU) is determined to accelerate the energy transition to renewable energy to, first, help climate-change mitigation and, second, increase energy security in the light of the Russian invasion of Ukraine. The successful transition away from fossil fuel-based energy, which is overwhelmingly imported, to renewable energy, which can be generated within the EU itself, would also help the EU achieve its ambition of achieving strategic autonomy. It is one of the key objectives of the current European Commission (EC) to achieve strategic autonomy in a more fragmented world.

The EC proposed the Fit for 55 initiative in mid-2021 to achieve its 2030 climate-change target of reducing carbon emissions by at least 55% from 1990 levels. As part of that initiative, the EC proposed to increase the share of renewables in EU final energy consumption from 22% in 2020 to at least 40% by 2030, as set out in an updated Renewable Energy Directive.

The Russian invasion of Ukraine has added urgency to the energy transition, with the EC presenting the REPowerEU action plan in May in response. As part of the action plan the EC proposed among other things to:

- increase the EU’s 2030 target share for renewables to 45% in final energy consumption, in other words twice as high as in 2020. For comparison, it took 16 years to double the share between 2004 and 2020. The REPowerEU Plan would bring the total renewable energy generation capacities to 1,236 GW by 2030, in comparison to the 1,067 GW envisaged under the original Fit for 55 initiative.

- accelerate the roll-out of photovoltaic energy as set out in the EU Solar Energy Strategy. This strategy aims to more than double solar photovoltaic capacity from around 160 GW now to over 320 GW by 2025 and a further near doubling to almost 600 GW by 2030. This frontloaded new capacity could displace the consumption of 9 bcm of natural gas annually by 2027. This is roughly 2% of EU natural gas consumption currently.

- exploit the opportunities available from wind energy by strengthening supply chains and accelerating permitting procedures.

With respect to wind energy, the REPowerEU action plan does not set any new targets beyond those already set out in the Fit for 55 initiative. The EU wants to increase wind energy capacity from 195 GW currently to ~500 GW by 2030, of which at least 60 GW should come from offshore installations. With the Esbjerg Declaration the governments of Belgium, Denmark, Germany and the Netherlands pledged in mid-May 2022 to meet around half of the overall offshore target through new capacity in their parts of the North Sea.

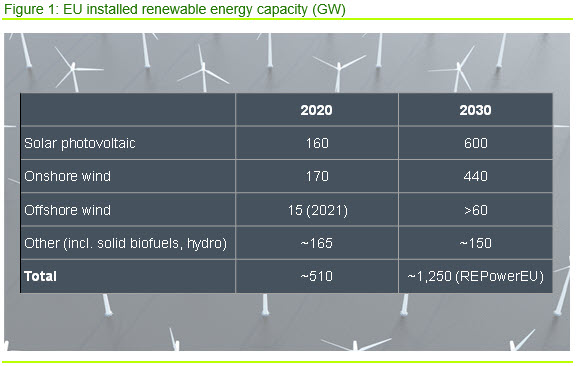

In terms of total renewables capacity, this translates into an increase from ~510 GW now to ~1,250 GW by 2030 (Figure 1).

DATA: European Parliament (2022), Eurostat Databrowser, CRU

The proposed increases equate to ~100 GW of new capacity annually over the next seven years (~9.3% annual growth on a compounded basis) compared with increases of ~40 GW in 2020 and 2021. In the case of wind power, that equates to ~40 GW new capacity annually over the next seven years – more than twice as much as is currently the case.

Are the EU targets realistic?

If achieved over the coming 7–8 years, these renewables targets would make the EU economy less reliant on imported natural gas and other fossil fuels and consequently more resilient against external shocks. They would also make an important contribution to meeting EU climate-change mitigation targets.

How realistic are they though, especially considering the current economic and financial circumstances as well as deep-rooted structural issues, such as those imposed by national planning legislation? In this section we look at the supply of inputs required to construct and install the planned capacity, the availability of funding and legal and regulatory factors.

THE COST OF RENEWABLE ENERGY HAS GONE UP AS MATERIAL PRICES HAVE RISEN

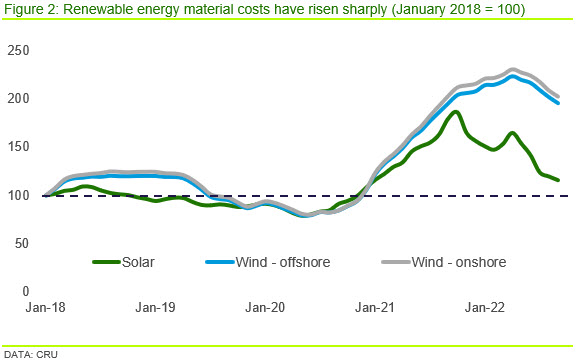

Renewable energy is highly materials intensive. As a result, the cost of adding new capacity is highly sensitive to material prices, which in turn depend on commodity and energy prices.

This is illustrated by the recent sharp increase in commodity prices during the Covid-19 pandemic and rapidly rising energy prices towards the end of 2021, which added significantly to the cost of renewable energy material (Figure 2). High energy prices matter as the metals required in renewable energy capacity are themselves energy-intensive to produce. For example, based on CRU’s proprietary cost data, fuel and power costs combined make up ~36% of costs for steel globally, 32% for aluminium and 24% for copper. The war in Ukraine has put further pressure on commodity and energy markets, adding to the cost of renewables.

DESPITE THE SHARP ECONOMIC DOWNTURN, THE AVAILABILITY OF SKILLED LABOUR WILL REMAIN AN ISSUE

Economic circumstances have deteriorated dramatically since the launch of the EC’s Fit for 55 initiative in mid-2021. At that time, it was expected that the European economy would recover from the deep recession caused by the Covid-19 pandemic and that accelerating inflation would prove to be temporary as global supply bottlenecks, also created by the Covid-19 pandemic, would dissipate.

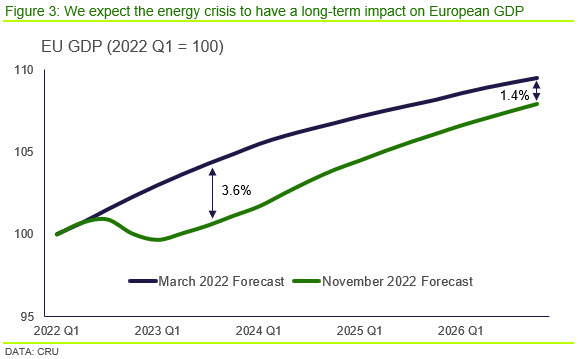

The Russian invasion of Ukraine in early-2022 has changed that outlook dramatically, with the energy crisis leading to a sharp slowdown in economic growth. We expect the EU to go into recession this winter, with only a partial recovery thereafter. As a result, economic activity could be ~1.5 percentage points lower at the end of the decade than it would have been without the current crisis (Figure 3).

So far, European labour markets have remained strong, with the EU unemployment rate falling to an all-time low of 6.1% in 2022 Q2 and labour shortages continuing to hold back businesses from expanding in numerous EU countries. We expect labour-market conditions to deteriorate in 2023 but not enough to significantly ease existing labour shortages. With the EU working-age population projected to decline sharply between now and 2030 and limited scope to encourage more workers to join the labour market, labour shortages will be a structural feature of the labour market for years to come.

Labour-market developments matter for the renewable energy sector as the manufacturing process and installation is labour intensive and requires skilled labour such as engineers and offshore construction workers. The renewable energy sector competes with the construction sector for these skilled workers.

Many EU countries have suffered from severe labour-market shortages in the construction sector over recent years, relying heavily on foreign workers to fill gaps. We expect the construction sector to weaken in the short term but to remain tight over the medium term. This means structural demand for labour from the construction sector as a whole is likely to remain strong for much of this decade.

At a minimum, this will require the renewables sector to compete for skilled workers in a tight labour market, which would drive up the cost of the energy transition. Even higher wage offers might not suffice to attract all the required skilled labour to meet demand though, in which case structural labour shortages could make it difficult for the sector to fully implement its expansion plans.

ENERGY MARKET INTERVENTIONS AND RISING BORROWING COSTS

Since the launch of the Fit for 55 initiative in mid-2021 there have been further dramatic policy developments in Europe. Most relevant to the renewables sector are the significant interventions in the European energy markets and the tightening of monetary policy after more than a decade of record-low interest rates as central banks try to address rapidly accelerating inflation.

A cap on electricity prices to support households over the short term

The governments of EU member states have launched a raft of measures to protect households and businesses from rapidly rising energy prices. EU member states are currently discussing a temporary EU-wide cap on wholesale gas prices used in electricity generation based on similar measures introduced by the Spanish and Portuguese governments in May 2022. The German government has offered a fiscal package worth up to €200 bn to soften the impact of higher energy prices on households and businesses, other countries have implemented similar (if less generous) policies.

As these policy interventions aim to lower the retail price below the wholesale price for electricity to support households and businesses deal with huge price increases, this policy intervention does not affect electricity producers themselves and as such should have no discernible impact on the renewables sector.

Revenue cap on inframarginal electricity producers

Another temporary measure is an EU-wide revenue cap on inframarginal electricity producers. This measure will be launched on 1 December 2022 and will initially be in place until 30 June 2023. Inframarginal electricity producers using nuclear and renewables – and to a lesser extent coal – have benefited from the high market price of electricity, which has been set by marginal producers using gas. This reflects the fact that the EU electricity market is based on a so-called merit order curve, which ranks the bids for next-day electricity generation according to increasing marginal cost of production.

The current high electricity prices are determined by the very high marginal costs of production faced by energy providers using natural gas. EU energy ministers decided to cap market revenues accruing to inframarginal producers at €180 /MWh. This is far below the peak wholesale electricity price of €500 /MWh recorded in August 2022 but higher than the wholesale price since September.

It has been suggested that the revenue cap could reduce the incentive to invest in renewables. However, while the market price remains below the revenue cap, this is a non-issue. Our analysis shows that even with a cap in place, investment should not be disincentivised. A cap of €180 /MWh is already well above the revenue required to provide adequate returns for an investment in the core renewable energy technologies. Moreover, as installation costs fall, a cap at this level will become even less relevant from an investment perspective.

Structural reforms to the European electricity markets

Several EU member states are also advocating more structural reforms to the EU energy market though not all member states agree on the issue. These reforms would be long term in their nature. The main objective would be to decouple the electricity price from the gas price by replacing the current merit order system with a new arrangement. This would mean that the electricity price would not need to increase in line with increases in gas prices in the future.

The EC set out in a non-paper ahead of the 25 October meeting of EU energy ministers how such an arrangement could look. It could be based on a contract for difference approach, which would offer a guaranteed price for non-fossil electricity producers. If the market price for electricity is higher, they would have to return the excess to governments, if the market price is lower, governments would compensate. According to the EC, such an arrangement would have to be complemented by a short-term mechanism, which ensured that the cheapest producers would still be used first – similar to the current merit order system. The EC has promised to present more detailed proposals in early-2023.

Major reforms to the energy market could potentially have significant implications for the future of the renewables sector, all the more so in the light of the recent increase in borrowing costs (see below). As long as the EU is genuine about the energy transition and achieving greater energy resilience, we would expect the long-term viability of the renewables sector to be a fundamental consideration in the design of a new arrangement.

That said, policy uncertainty is a key investment risk and a transparent and predictable business and investment environment will be required for the EU energy transition to become a reality. We explored policy-related risks in our recent insight on Spanish solar auctions.

Rising financing costs pose a challenge

The second major economic policy development affecting the renewables sector are rising interest rates and borrowing costs as central banks try to address rapidly accelerating inflation. The European Central Bank (ECB), which is in charge of monetary policy in the euro area, raised its key policy rate to 1.25% in September and then to 2.0% in early-November – the highest in more than a decade. We expect the refinancing rate to reach 3.0% in the first quarter of 2023 and to remain there through the year.

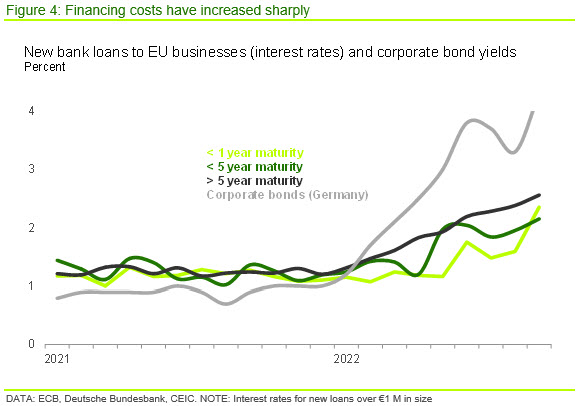

Tightening monetary conditions are being reflected in higher borrowing costs for bank loans to businesses (Figure 4). Longer maturity loans began to rise first from end-2021, reflecting higher bond yields. In recent months, shorter maturity rates have increased the most sharply as the ECB has tightened policy.

Corporate bond yields in the capital markets have also increased sharply since early-2022, with corporate bond yields in the German industrial sector, for example, rising from ~0.5% in January to ~4.0% in November.

The impact of higher borrowing costs will be felt across the whole economy but will be particularly pronounced in the renewables sector given its significant up-front capital expenditure and generally long pay-back periods spanning decades. We have estimated that a 100 bp increase in RoR leads to a 10% increase in the levelised cost of electricity required to break even. The sharp increase in borrowing costs can therefore be expected to slow the installation of renewable energy capacity. This needs to be considered in any proposed reforms to the EU energy markets.

DEVELOPING CAPITAL MARKETS – FUNDING THE ENERGY TRANSITION

Rising borrowing costs should hold back investment in renewables, but there is more to funding than the cost of capital. Crucially, businesses need ready access to funding to pursue their projects. Given the huge amounts of money involved, this will require private-sector involvement.

CRU analysis suggests that an average of €95 bn will be required per year up to 2030 to meet the EU’s renewable energy targets at current costs. Additional investment would be required in storage capacity.

Establishing a single European market for capital has proved difficult

Nearly 15 years after the Great Financial Crisis, European businesses continue to rely heavily on banks to fund their projects. In 2014, the then EC launched the Capital Markets Union (CMU) project aimed at establishing a single EU market for capital. It was hoped that CMU would reduce European businesses’ dependency on bank lending – thereby increasing resilience of the real economy to financial market shocks – and make capital allocation across EU member states more efficient. Since then, there has been only limited progress on CMU, with the harmonisation of financial services across EU member states proving far more challenging than initially imagined. The current EC, which came into office in 2019, relaunched the initiative in 2020 (“CMU 2.0”) with little effect. The lack of a single EU market for capital is seen as holding back the EU’s growth potential and might make it more difficult for businesses, particularly in the EU’s peripheral countries with their generally smaller domestic capital markets, to secure funding at attractive conditions. In 2021, European policymakers floated the idea of a Green Capital Markets Union (GCMU), arguing that the green transition could provide the impetus needed to establish the CMU, which in turn was needed to finance the transition. Given previous challenges, we do not expect any major progress on GCMU over the coming years.

Solid progress on developing the Sustainable Finance Framework

By contrast, the EU has made solid progress on its Sustainable Finance Framework over recent years. This should facilitate the flow of private-sector capital into green projects, including renewables.

The framework builds on three pillars: the EU taxonomy for sustainable activities; comprehensive disclosures for financial and non-financial institutions; and a toolbox to develop sustainable investment solutions.

- The EU taxonomy for sustainable activities was established to channel financial resources into green activities, including investments in the renewables sector. The taxonomy provides companies, investors and policymakers with definitions for which economic activities can be considered environmentally sustainable. Controversially, in March 2022 the EC decided to include, under strict conditions, specific nuclear and gas energy activities in the list of economic activities covered by the taxonomy. Critics of this decision have suggested that this could result in a lack of funds going into the renewables sector. The taxonomy has also been criticised for not doing enough to prevent greenwashing.

- In mid-November, the European Parliament adopted the EU’s Corporate Sustainability Reporting Directive that obliges companies to disclose information on their societal, governance and environmental impact across the value chain. EU member states are expected to adopt the directive on 28 November, which will cover nearly 50,000 companies in the EU.

- The third pillar is a toolbox to develop sustainable investment solutions that could prevent green washing. In mid-2021, the EC proposed the development of a European Green Bond Standard (GBS) that could eventually replace existing market-based or industry group standards. The European Parliament and EU member states are currently discussing the details of a European GBS, which could be launched in 2023 or 2024.

EU investors have embraced environmental goals more than others, with many members organised in the Glasgow Financial Alliance for Net Zero representing financial institutions committed to accelerating the energy transition based in Europe. We expect EU banks and capital markets will be able to provide the significant funds required to finance renewable investments over the coming years even though continued market inefficiencies are likely due to the missing single market for capital.

THE EUROPEAN COMMISSION WANTS TO SIMPLIFY AND ACCELERATE PLANNING AND PERMITTING PROCESSES

There is also the planning system to consider, which is an obstacle to the rapid rollout of renewable energy sources in the EU. In 2020, the EC established the ‘Renewable Energy Simplify (RES) project to identify ways to simplify the permission and administrative procedures for renewable energy installations. The project will conclude in April 2023. The RES Interim Report published in May 2022 suggested that nearly half of the barriers to investment in EU renewables projects were the result of administrative and grid issues, most notably the lack of legal coherence, incomplete frameworks, conflicting public goods and the lack of support from policy makers and institutions. Such barriers have resulted in lead times of up to 10 years for renewable projects. The report argued that if the REPowerEU target of 45% renewables is to be achieved by 2030, substantial legislative changes to the planning system are required immediately. This is a particular challenge for the EU as planning and permitting legislation is within the competency of member states rather than on the EU level, with little to no coordination.

To counter this problem, the EC has proposed measures to speed up permit-granting along with specific frameworks for permit-granting procedures. Under the proposal, all EU member states would be required to designate locations suitable for renewable projects as “go-to areas”. Under the proposed framework, the permit-granting process for “go-to areas” should not exceed one year for any project, six months for projects with an electrical capacity of less than 150 kW and three months for solar energy projects. The time frames are longer for projects in areas not designated as “go-to”. If an authority fails to issue a decision within the given time frame the permit should be granted automatically.

The EC published a revised version of the Renewable Energy Directive IV (RED IV) in September, which includes the REPowerEU “go-to” renewable areas and accelerated permit-granting. At the time, the EC proposed that the planning and construction of renewable projects should be considered as an overriding public interest when balancing legal pursuits.

In the EU, it is the responsibility of the EC to propose legislation and for the EU member states and the European Parliament to legislate. This can be a lengthy process. Citing the urgency of the matter, the EC tabled a temporary emergency regulation in mid-November to speed up the permitting process until RED IV has been legislated for. It is currently unclear whether the member states will support the proposed RED IV in its current form given previous domestic opposition to major infrastructure projects. We expect the final version of the directive will be watered down from the EU proposal.

Reaching the targets will be challenging

Meeting the EU’s ambitious renewable energy targets will be a challenge for a myriad of reasons. For a start, material and energy prices have risen sharply since the outbreak of the Covid-19 pandemic, driving up the cost of new renewables installations. The war in Ukraine has driven up costs further. Similarly, rapidly rising financing costs can be expected to slow the installation of new capacity.

Beyond costs there are other factors that are likely to hold back the installation of new renewable capacity, including structural labour-market shortages in much of the EU, policy uncertainty and national planning and permitting systems. The latter are widely recognised as an obstacle to the rapid rollout of renewables across the EU, with the EC proposing major changes to accelerate and simplify processes. Given that planning and permitting falls with the competency of individual member states, progress will be difficult to achieve.

Despite the significant sums required to fund the energy transition, gaining access to financing might turn out to be one of the smaller challenges even though the lack of a single market for capital in the EU might disadvantage more peripheral countries with smaller domestic capital markets.

In conclusion, even with the best of their intentions, EU policymakers will find it difficult to meet their ambitious 2030 renewable targets.

Find out more about our Sustainability Services.

Our reputation as an independent and impartial authority means you can rely on our data and insights to answer your big sustainability questions.

Tell me more