Solar prices from Spain’s first renewable energy auction in 2021 Q1 has led investors to believe that very cheap solar is finally here. However, while solar energy has become cheaper, these auction prices do not reflect full costs and it is misleading to use them as indicators of solar costs today.

CRU’s view is that developers used the auction primarily to secure the grid connection and took on sizeable risk in the hope of generating profits once the auction contracts ended, after 12 years. We believe bidders estimated that higher electricity prices in the mid-2030s, driven by higher carbon prices, would compensate them for low contract prices today. While rising carbon prices favour their calculations, recent policy developments in Spain could jeopardise the profitability of these projects.

Solar is not as cheap as the auctions suggest

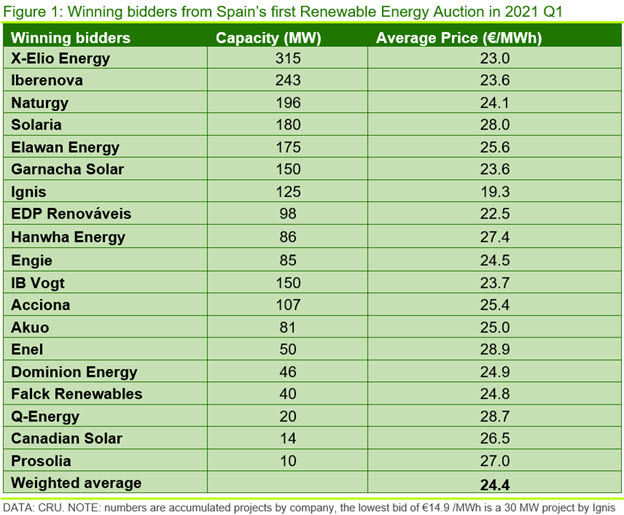

Spain hosted its first renewable auction in January 2021, in which the Ministry for Ecological Transition awarded contracts to 3 GW of renewable energy projects. More than two thirds of those were granted to solar PV projects and winning bids were offered a 12-year power purchase agreement (PPA). The average successful bid price was €24.5 /MWh, but winning bids went as low as €14.9 /MWh. While this auction represents less than 1% of Spanish energy demand and less than 14% of Spanish solar capacity, these bids have been quoted as signals that solar costs continue to fall rapidly. But do these bids reflect the real cost of solar energy? We would argue they do not for two reasons.

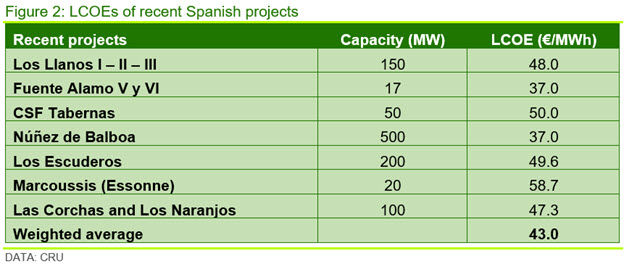

Firstly, recently commissioned projects do not justify the low bid prices. The following Spanish projects have been commissioned since 2020 and their levelised cost of electricity (LCOE) are significantly higher than the winning bids, much in line with CRU’s solar LCOE estimation. That is, while the average winning bid was €24.4 /MWh, the average LCOE of recently commissioned projects is ~€43 /MWh.

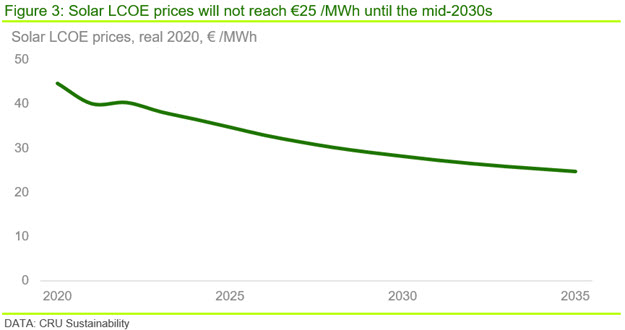

Secondly, the past five years have seen a flattening of the solar LCOE curve compared to the sharp declines between 2008 and 2015 and, while we expect solar prices to continue fall, the rate of decrease will be slower. Given that the winning projects must be commissioned by 2024, our analysis suggests a price of ~€40 /MWh (real 2020) would be required to achieve breakeven – before taking account of recent inflation – well above all the bids awarded a contract. That is, the revenue of the winning projects cannot cover the necessary CAPEX, let alone OPEX, and so, on their own, these levels of revenue cannot generate sufficient profit to justify the investment. So, what is happening?

Auction contracts offer flexibility, but are still too low

The Spanish government offers a special kind of PPA via its auction process, termed a partially symmetric contracts-for-difference (CfD). A partially symmetric CfD requires the generator to provide the offtaker (i.e. the government) with a certain amount electricity at the bid price but, if the generator does not produce the required minimum, it can be penalised. Thus, while a partially symmetric CfD eliminates some risk, such as providing grid connectivity and ensuring a certain level of revenue, at the same time it locks in low, unprofitable rates for the generator and some penalties for under performance. However, as the amount of electricity covered under the CfD is capped, everything that the solar farm produces above that amount can potentially be sold at a more favourable price through a traditional PPA.

Having said that, the average price of a traditional solar PPA in Spain was ~€39.5 /MWh in 2022 Q2, which is also below CRU’s current solar LCOE for Southern Europe of ~€43 /MWh. So, if generators split their production equally between their CfD and a traditional PPA, that will still only provide an average revenue of ~€32 /MWh for participants of the first auction, well below that required to cover full project costs and provide a return.

We believe a key factor here is the provision of grid connectivity.

Renewables lead to significant additional costs associated with grid balancing – that are typically ignored in much analysis of renewable costs – and these are significant and will ultimately need to be borne by the consumer. As such, access to the grid needs to be managed and cannot be offered to any and all developers that wish to build a renewable plant. We believe this restricted access provides an incentive to project developers to bid low prices in the auction process as explained below.

Are developers playing game theory on a large scale?

Given the apparent unprofitability of these projects at the bid prices offered, we conclude two things. First, the easiest and most guaranteed way to secure grid connection is through government contracts, which would explain the developers’ low bids to ensure projects can go ahead.

Second, developers would not progress these developments if they did not believe they could make sufficient profit over the lifetime of the project. The CfD will be in place for about half the lifetime of a project. Therefore, generators must be assuming they can make up the losses incurred during the first 12 years, which necessarily means they expect higher electricity prices after the CfD is finished.

Our analysis suggests, for the average bidder, the wholesale electricity price would need to be ~€89 /MWh on average throughout the second half of the project lifetime for break even and, for the lowest bidders, it would need to be ~€116 /MWh, both massively higher than the winning bid prices. This is important as it indicates how these project developers believe electricity prices will develop over the next 25 years.

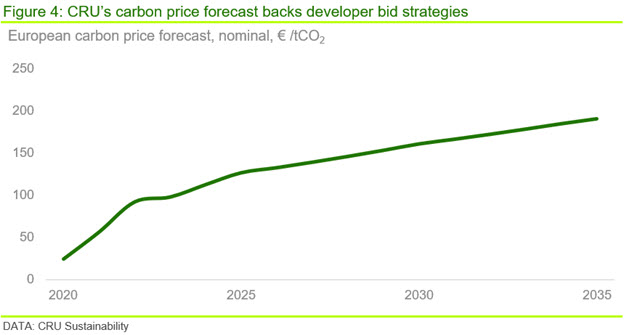

Outside of the current energy crisis – which would not have been a consideration when these bids were finalised – carbon price (i.e. the EUA price in Europe) is expected to be the main driver of electricity prices in Europe in the 2030s. Further, the electricity prices required to ensure these projects are viable imply an EUA price of ~€85 /tCO2 for the average bid price projects and ~€151 /tCO2 for the lowest bid project, assuming underlying energy costs are close to historical steady-state levels.

At the point at which these bids will have been finalised (i.e. 2020 Q3) the EUA price was ~€27 /tCO2 but it has since lifted to ~€85 /tCO2. CRU forecasts that the EUA price will lift to ~€140 /tCO2 (real 2020) by 2036, when the CfD payments to these projects will end and they will be exposed to the wholesale price at that point.

If our forecast proves to be correct, those projects that bid close to the average auction price of ~€25 /MWh will see very strong returns over the lifetime of the project and would suggest that the Spanish government has undersold the value of grid access in these cases. Even the lowest bidding project should be in the money, although there is much less headroom for the carbon price to deviate very far from our forecast. If energy prices remain elevated, then a combination of higher energy and carbon prices should ensure these projects are profitable over their lifetime.

Severe risks are involved

The long lifetime of these projects and the lock in of low prices in the early years engenders risk, but this appears to have been more than adequately mitigated by most of the project promoters. However, we believe there are other risks factors that may not have been considered, primarily because they have only come to light since the auction process.

That is, fossil fuels have typically acted as the price-setters for wholesale electricity markets in Europe and auction bids will almost certainly have been predicated on continuation of this pricing mechanism. However, earlier in 2022 and considering soaring wholesale electricity prices resulting from the current energy crisis, Spain, along with Portugal, agreed with Brussels to introduce a temporary price cap on natural gas to decouple electricity prices from fuel prices. More broadly, other governments have questioned the merit order approach to electricity price setting in the wholesale market.

If Spain’s attempt to decouple electricity prices from fossil fuel prices is deemed to be successful, this could jeopardise the long-term profitability of the winning projects if that leads to policy change. If perceived to be realistic, such potential policy changes could result in the abandonment of projects before they are built, given the deadline for commissioning is 2024.

Solar costs declining, carbon price on the rise

Solar costs have been falling and we expect solar costs to continue to fall but recent auction bid prices in Spain – which many people are referencing as an indication of just how far solar costs have fallen – do not reflect full costs of solar. Rather, low bid prices more closely reflect the degree to which project developers are prepared to underbid (i.e. compared to full costs) to get access to the grid today in the expectation that they can earn excess returns in 12 years’ time, once CfD agreements with the government expire.

This approach is not without risk for the developers, but it is predicated on carbon prices rising and the continuation of the merit order approach to price setting in the electricity wholesale market. However, attempts by the Spanish government to move away from the merit order approach could undermine the rationale and could lead to project cancellations if it looks like becoming a longer-term policy.

We expect carbon prices to grow rapidly in the coming years and, assuming no significant policy changes, these projects will provide a return. However, the bid prices published should not be taken as a measure of costs of solar today.

If you would like to discuss this insight in more depth or learn more about CRU’s carbon emissions analytics, do not hesitate to get in touch with us.

Find out more about our Sustainability Services.

Our reputation as an independent and impartial authority means you can rely on our data and insights to answer your big sustainability questions.

Tell me more