Part three of our three-part Insight series covers the impact on commodity markets

China, the USA and Europe are pursuing different strategies to establish their leads in future green markets. In mid-2022, the US government launched the Inflation Reduction Act (IRA). EU policymakers are concerned that the financial support to US-based green businesses offered by the IRA could make Europe relatively less attractive as a green-tech location, adding to pressure from Chinese competitors. With a Green Deal Industrial Plan, EU policymakers now want to level the playing field by promising faster permitting, better funding, skilled workers and resilient supply chains. EU subsidies to green businesses would be costly to European governments but could also lead to new green innovations and capacity building in green technology and production beyond what could be achieved by the IRA alone.

In the final part of our Race to dominate future green markets Insight series, we assess the likely impact of the latest global policy developments on the green transition in general and on commodity markets in particular.

In part one of this series, we looked in more general terms at the policy options available for countries to compete in the race to dominate future green-tech markets. In part two we covered the EU Green Deal Industrial Plan and supplementary acts in more detail.

Aligning the EU Green Deal and US Inflation Reduction Act

The US Inflation Reduction Act on its own will not suffice to drive the energy transition

Climate change is the result of a market failure that allowed economic activities to take place without taking account of the environmental costs involved. Mitigating climate change will require sustained investment in new green technologies and renewable energy capacity over several decades.

As argued in part one and part two of this Insight series, the US Inflation Reduction Act (IRA) can be seen as a game changer in the global response to climate change. However, as substantial as the financial incentives offered by the US IRA are, they will not suffice to drive the energy transition on their own.

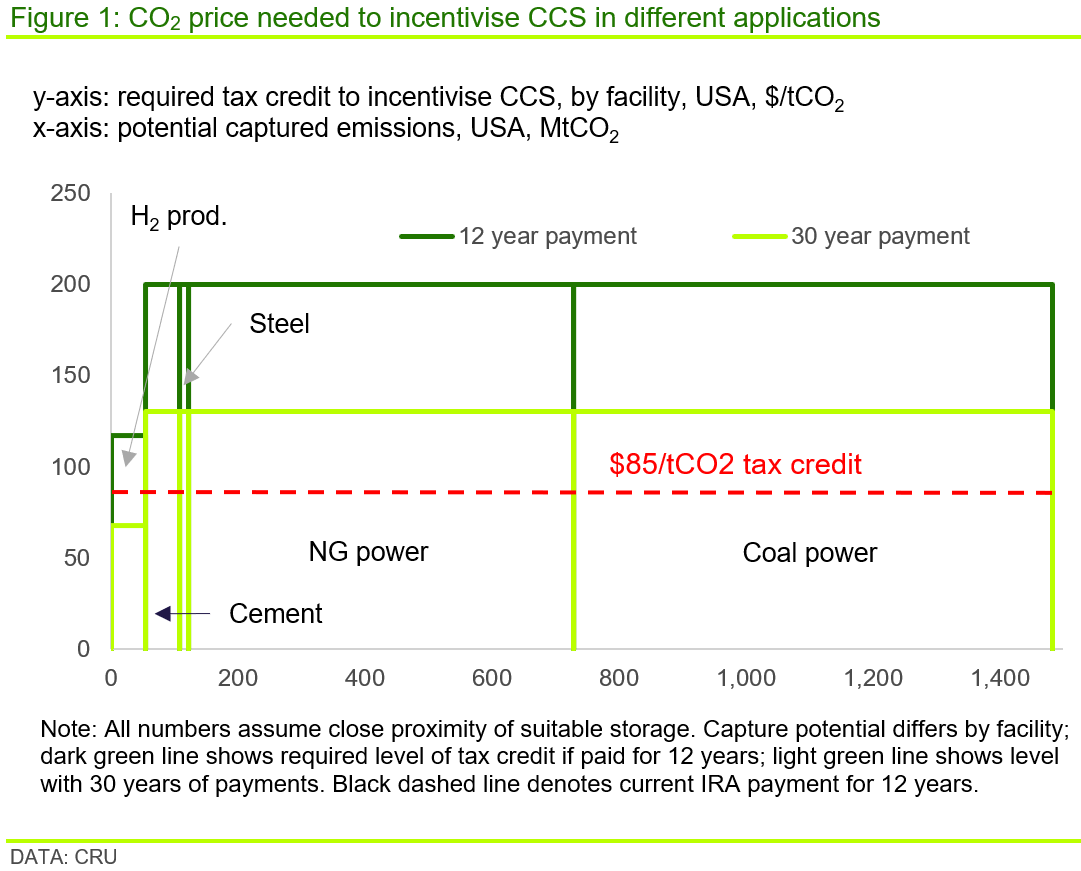

For example, to incentivise deployment of CCUS solutions, federal tax credits (n.b. often referred to as ‘45Q credits’) offered as part of the IRA provide up to $85 per tonne of CO2 that is permanently stored – a significant amount, but not enough to cover the true costs for most CCS applications as Figure 1 shows.

Figure 1 shows the required tax credit needed to incentivise CCS in different applications based on payments over 12 years (n.b. the actual duration of Q45) and 30 years (n.b. a realistic lifespan for this type of project).

Figure 1 shows that the current policy of a tax credit of $85/tCO2 offered over 12 years (n.b. shown in the figure by the red dotted line) on its own is too low to incentivise CCS in any application. To incentivise CCS in all but the hydrogen sector, the tax credit would have to be around $200/tCO2 over 12 years – more than double what it is now. It would have to be ~$125/tCO2 for hydrogen. Even if the tax credit was paid over 30 years, the amount available would only be enough to incentivise CCS in hydrogen production.

From competition to complementarity?

European policymakers were initially mainly concerned that the significant financial incentives offered by the US IRA could lead to a loss in competitiveness vis-à-vis the USA. Over recent months European policymakers have risen to this challenge though by developing more ambitious policies themselves, culminating in the promise to match aid in exceptional circumstances as set out in the Temporary Crisis and Transition Framework. There is a sense that addressing the climate change challenge is not a zero-sum game – all regions can and must play a part in this.

In this regard the US IRA has already left its mark by encouraging EU policymakers to provide their own financial incentives, thereby raising the aggregate amount of financial incentives available to green-tech businesses globally. A similar policy response can be seen elsewhere, with the Canadian government launching its own financial package aimed at the green-tech sector as part of its 2023 budget on 28 March, the French government setting out its own green industrial plan and the South Korean government currently considering its own financial options to accelerate the country’s green transition.

The meeting of US President, Joe Biden, and the President of the European Commission, Ursula von der Leyen, on 10 March marks a step change in this regard. They stressed the need to align EU and US policy approaches and invest to build green-tech economies and industrial bases and announced the launch of a Clean Energy Incentives Dialogue to coordinate the respective incentive programmes so that they are mutually reinforcing. Moreover, they promised to take steps to avoid disruptions in transatlantic trade and investment flows that could arise from their respective incentive programmes (i.e. the initial EU concern) and design incentives in such a way that they would maximise green-tech deployment and jobs.

A critical minerals club as a blueprint for closer cooperation?

With EU policymakers keen to ensure that European businesses can benefit from US green-tech financial incentives, it is likely that they will offer reciprocity by making available EU financial incentives to US businesses as well. This would create an EU-US market for green-tech businesses with access to aligned policies.

One obstacle to establishing such a ‘club’ could be the World Trade Organisation’s most favoured nations rules, which require countries to grant the same trade conditions to all countries outside formal free trade agreements (i.e. trade without discrimination). The USA and EU do not have a free trade agreement. That said, the WTO rules focus on more traditional trade barriers such as import quotas and tariffs – more recent policy developments such as corporate sustainability reporting across global supply chains are not captured by WTO rules.

Current discussions between EU and US policymakers therefore suggest a way forward. At their meeting in mid-March, Joe Biden and Ursula von der Leyen also announced that the USA and EU would be working on an agreement to boost domestic mineral production and processing and expanding access to sources of critical minerals that are sustainable, trusted, and free of labour abuses. Moreover, they stressed that closer cooperation would be necessary to reduce strategic dependencies in the relevant supply chains and ensure they are diversified and developed with trusted partners.

In addition to the EU and US, the other G7 countries Canada, Australia and the UK are currently revising their critical mineral strategies with the aim of reducing strategic dependencies and strengthening supply chains. The Japanese government addressed these issues in the Economic Security Promotion Act in 2022. On 14 March the European Commission, for example, set benchmarks for domestic capacities along the strategic raw material supply chain and to diversify EU supply:

- At least 15% of EU annual consumption for recycling.

- At least 10% of EU annual consumption for extraction.

- At least 40% of EU annual consumption for processing.

- Not more than 65% of the EU annual consumption of each strategic raw material at any relevant stage of processing from a single third country.

Meeting these targets will not be easy. For example, domestic nickel and cobalt extraction currently only meets ~6-7% of EU consumption, while nickel processing is equivalent to ~14% of EU consumption – less than half the target.

We expect G7 countries to publish their own respective targets over the coming year and start cooperating more closely on the sourcing of critical minerals. Such cooperation could be the first step towards the formal launch of a critical minerals club – in principle open to all countries but in practice limited to those that meet the strict membership criteria – that could evolve into a more general G7 green-tech club over time.

What does the race to dominate future green markets mean for the commodity markets?

Regardless of whether the EU, USA and other advanced economies will ultimately be able to meet their ambitious climate-change targets, the sharp increase in financial incentives on offer to accelerate the green transition and the expected closer cooperation among advanced countries on critical minerals will have a profound impact on commodity markets.

The first impact concerns timing: demand for commodities required for the energy transition will increase more rapidly than previously expected. The second impact concerns location: a greater focus on supply chain resilience in G7 countries will dictate future production locations and therefore investment decisions.

Demand for commodities required for the energy transition will increase much more quickly than previously expected

Substantial financial incentives and other policy initiatives such as faster permitting should bring forward the increase in demand for green tech by many years. Consumers are incentivised or legally required to purchase green products and technologies such as electric vehicles and residential heat pumps as governments try to decarbonise the transport and residential building sectors, while businesses are incentivised or legally required to invest in green production facilities and focus on green products.

To meet this rapid increase in demand, commodity producers will have to scale up production more quickly than previously planned. For example, if current targets for renewable energy installations by 2040 are brought forward to 2030 within the EU, this would require an extra ~50 Mt of steel to the end of the decade, in addition to the current expected demand from renewables installations to 2030 of ~45 Mt; so more than doubling requirements.

Faster permitting would also open the way to accelerated installation of renewable energy sources within the EU, in particular on- and offshore wind. This would lead to a more rapid increase in demand for raw materials required in the production of windfarms as long as the required skilled labour is available as well.

Critical mineral targets in advanced countries will require shifts in exploration and investment

Commodity producers will also need to adapt to the G7 countries’ domestic targets for critical raw materials and strategic raw materials production, with supply chain resilience likely to dominate more straightforward cost and efficiency considerations. Meeting these targets will require a significant increase in domestic production capacity, which will have a major impact on the regional breakdown of future exploratory activities and investment decisions.

Standards for mining and commodities are particularly high in advanced countries

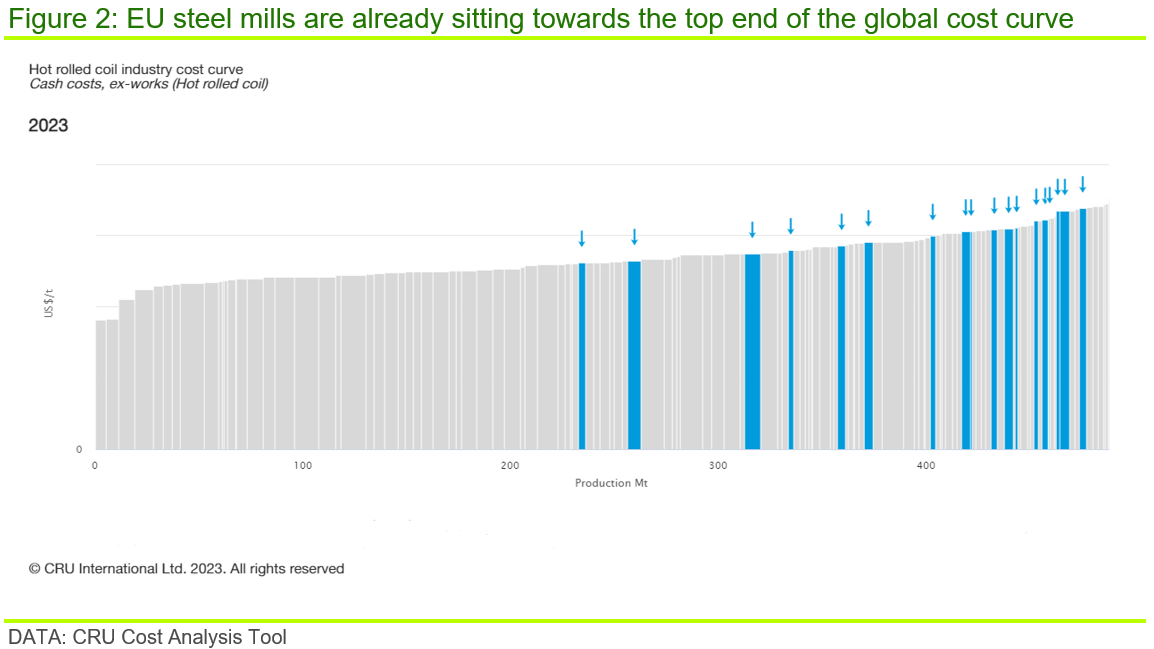

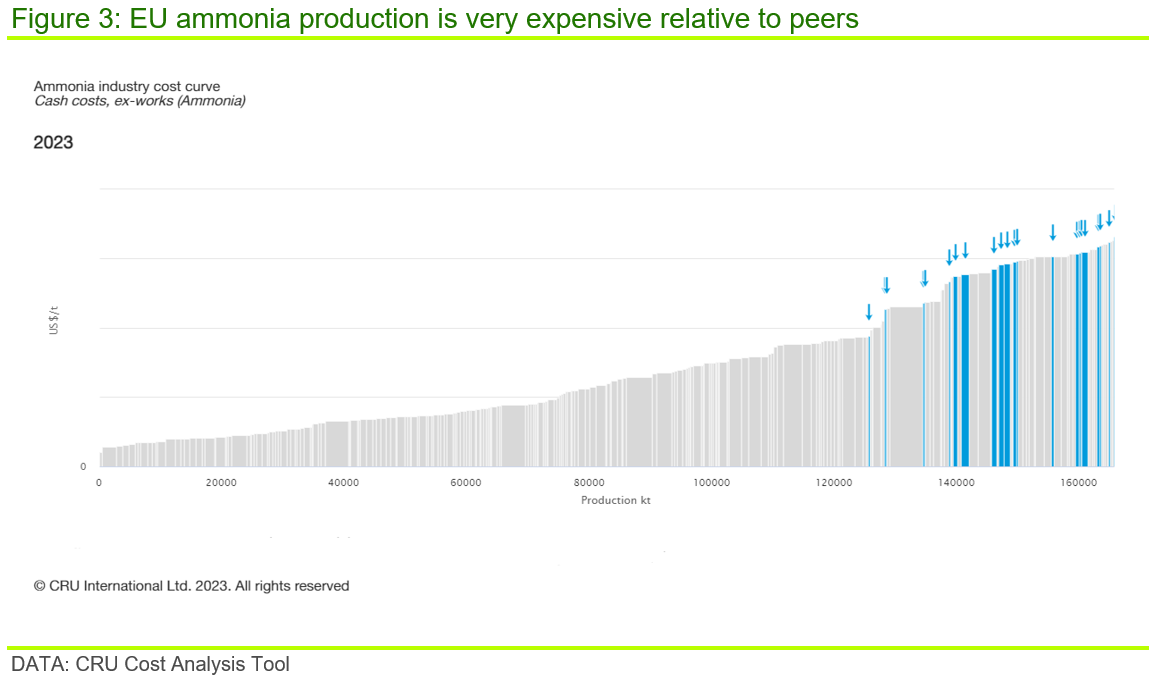

Commodity producers will also need to adapt to the generally higher environmental, social and governance standards in G7 countries than in much of the rest of the world. This poses particular challenges on the local and national level, with the mining impact on local biodiversity or water, for example, a particular concern in much of the EU. Similarly, commodity producers can expect tougher scrutiny on corporate governance and accountability and will need to deal with generally higher labour standards (e.g. in terms of health and safety regulation) and costs such as wages and social security contributions. While the EU Corporate Sustainability Reporting Directive will require businesses along global supply chains to improve their reporting standards, requirements will most likely remain higher in the G7 countries themselves. All of this will make mining, steel production and other activities more expensive than in other locations.

Figures 2 and 3 illustrate this for steel and ammonia production, with European production facilities highlighted in blue. Figures 2 and 3 show that European steel and ammonia production is already at the upper end of the global cost curve. It is likely that European facilities will move even further up the global cost curve over time.

It is too early to say whether these increased costs can be passed on fully to consumers, potentially requiring cost savings elsewhere or hitting profitability.

The above does not mean that existing production capacity in other parts of the world will become redundant. Demand for critical minerals will increase rapidly elsewhere as well, including China, the third competitor in the race to dominate green tech in the future.

It does imply though a partial geographic reconfiguration of supply chains, with a smaller share of critical mineral production in non-G7 countries going to G7 countries than in the past.

More to come

The 2022 US IRA marks a turning point in addressing global climate change. For the first time significant financial incentives are available in the USA to accelerate the energy transition. Moreover, it has encouraged other countries to follow suit. This will have brought forward the energy transition by many years.

We expect that governments will commit further significant sums to this over coming years, with targeted government spending and tax credits seen as a necessary investment to incentivise private-sector action and avert a climate crisis. The commodity markets will need to be ready to keep up with this accelerated pace of change over the next decade.

To discuss any of the issues covered in this or any of our previous Insights please reach out to CRU Sustainability.

Find out more about our Sustainability Services.

Our reputation as an independent and impartial authority means you can rely on our data and insights to answer your big sustainability questions.

Tell me more