EU ETS and CBAM progress, as China unveils its improved industrial energy efficiency plan

Catch up on the latest in our new policy-focused regular report

Dealing with climate change might seem like a luxury in times of geopolitical tensions but this hasn’t stopped European and Chinese policymakers making progress on some of their flagship climate policies. In June, European policymakers made a big step towards launching a revised EU Emissions Trading Scheme and a Carbon Border Adjustment Mechanism by 2023. Meanwhile, the Chinese government focused its attention on raising the energy efficiency of the Chinese industry. June also saw a number of developments in the area of green finance – from addressing the risk of greenwashing to issuing more green bonds. Watch this space.

Summary

In the July 2022 Policy Roundup, we discuss:

- progress by EU policymakers on revising the EU Emissions Trading Scheme (EU ETS) and introducing a Carbon Border Adjustment Mechanism (CBAM) despite geopolitical headwinds. These should become law by early-2023, leading to higher carbon prices for EU producers and their non-EU competitors selling into the EU.

- the Czech EU presidency’s focus on energy security in light of the war in Ukraine, with the Czech government keen for the EU to adopt the European Commission’s recent REPowerEU proposals.

- the European Parliament’s vote in favour of including certain natural gas and nuclear activities in the EU taxonomy on sustainable activities – despite strong opposition from a number of EU member states. Whether asset managers will invest in these activities remains to be seen.

- the latest corporate sustainability reporting directive, which will require most EU-based businesses to report on environmental, social and governance factors over coming years. EU policymakers hope that the new directive will reduce the risk of greenwashing.

- the Chinese 2025 energy industrial efficiency improvement action plan published at the end of June, which includes market-based instruments and realistic targets. We expect China will achieve its industrial energy efficiency target by 2025 as it is not particularly ambitious.

- the 2025 hydrogen development plan published by Tangshan city government. The detailed plan and the momentum of seeking a green transition should allow Tangshan to achieve its hydrogen development goals despite the significant financial commitment required.

- the issuance of green bonds by six Chinese state-owned enterprises in energy-intensive industries issued medium-term corporate green bonds in June to finance investment in low emissions technology with low financing costs.

European Union

European lawmakers progress on revised ETS and CBAM

In June, European lawmakers made progress on a revision to the European Union’s Emissions Trading Scheme (EU ETS) and the introduction of a Carbon Border Adjustment Mechanism (CBAM).

As part of its ‘Fit for 55’ package, in July 2021 the European Commission (EC) proposed major revisions to the EU ETS and the introduction of CBAM, the latter to create a level playing field between producers located within the EU and foreign competitors. It is for the EC to propose new policies but for the European Parliament and the member states – represented in the Council of the European Union (Council) – to legislate.

The European Parliament and the Council agreed on their respective positions on a revised ETS and CBAM in June. This means that the two parties are now in the position to negotiate the final legislation in the second half of this year. CRU expects that this will be completed by year-end, with the new legislation coming into force from 2023 onwards.

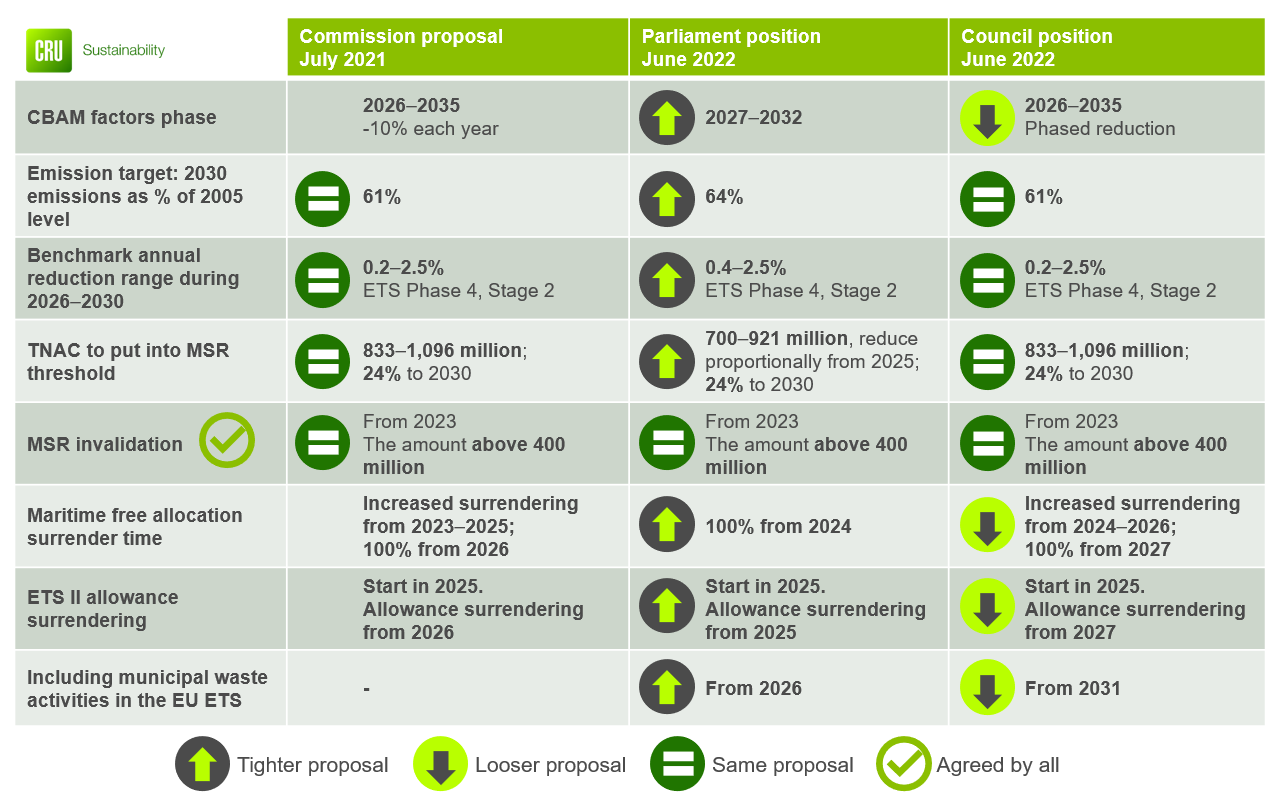

While the European Parliament and the Council have currently slightly different positions on aspects of a revised ETS and CBAM – and both deviated in several ways from the original EC proposal – it is important to note that both parties agree on a revised ETS and the introduction of CBAM in principle. This means that the ETS will cover more economic activities and will have a higher carbon price in the future. Policymakers are also keen to launch a second ETS – ETS II – to operate alongside the existing one. ETS II would cover road transport and housing, and would have a slightly less ambitious carbon reduction target up to 2030 than the existing ETS. It has been proposed that the two schemes could be merged in the future. The final legislation will likely involve several compromises reflecting current negotiation positions. Table 1 below summarises the main positions.

Figure 1: The European Parliament’s and the Council’s positions on EU ETS and CBAM

DATA: European Commission, European Parliament, Council of European Union

DATA: European Commission, European Parliament, Council of European Union

The Czech EU Presidency prioritises energy security

The Czech Republic took over the Presidency of the Council of the EU (EU presidency) from France in early-July. The presidency rotates between EU member states on a six-month basis. The Czech government has made it clear that the energy transition remains a policy priority over the coming months, with the war in Ukraine adding to the urgency to invest in renewables. As such, the Czech government is keen the EU adopts the EC’s proposed REPowerEU package (published in May) as quickly as possible. The overarching objective of REPowerEU is to rapidly reduce the EU’s dependence on Russian energy imports. The EC proposes to achieve this by energy savings, diversification of energy supplies (e.g. in the form of liquid natural gas) and the accelerated transition to renewable energy sources in homes, industry and power generation. We expect the EU to adopt this package over coming months.

Running the EU presidency is one of the most important ways for EU governments to directly shape the EU policy agenda for the coming six months.

EU taxonomy on sustainable activities to include certain natural gas and nuclear activities

The EU taxonomy on sustainable economic activities is meant to guide private investment to activities that can help the EU achieve its climate change ambitions. In February, the EC presented a so-called complementary climate delegated act in which it proposed to include certain natural gas and nuclear activities in its taxonomy. Justifying its proposal, the EC argued that it was a pragmatic and realistic approach to helping EU members transition to a low carbon economy. More recently, the EC argued that the need to reduce the EU’s dependence on Russian energy imports made that inclusion even more important. The proposal was backed by France and several central and eastern European member states but strongly opposed by others, including Germany, Austria and Luxembourg, which argued that it would send the wrong signals to the financial community and could starve the funding for genuinely green investments.

On 6 July, the European Parliament voted in favour of the EC’s proposals, which means that the delegated act can enter force in January 2023 – EU member states do not have a veto right on delegated acts.

A new reporting directive to address greenwashing concerns

Whether the inclusion of certain natural gas and nuclear activities in the EU taxonomy will have any major impact on the actual asset allocation of institutional investors remains to be seen. European financial markets have been hit by several high-profile greenwashing scandals over recent months, with many investors concerned about reputational risks from investing in nuclear technologies.

To address greenwashing concerns, the European Parliament and the Council reached a provisional political agreement in mid-June on a new corporate sustainability reporting directive (CSRD). It will require businesses to provide more detailed reporting on sustainability issues, including environmental, social and governance factors. Moreover, businesses will have to adhere to new certification requirements for sustainability reporting and offer improved accessibility of information. The directive will apply to all large companies already subject to the 2014 non-financial reporting directive, and all companies listed on regulated markets from January 2024 onwards. Coverage will be extended to all large companies currently not subject to the non-financial reporting directive from January 2025 onwards and then eventually certain small- and medium-sized enterprises from 2028 onwards. The directive will also apply to non-EU companies with a net annual turnover of €150 M in the EU and at least one subsidiary or branch in the EU.

We expect that EU initiatives such as the taxonomy on sustainable activities and the new CSRD will help to mainstream green finance, with other countries introducing similar measures over coming years.

China

In China, energy efficiency targets do not appear to be particularly onerous for the industry, and it will be supported by a detailed plan and low-cost financing channels.

China to improve industrial energy efficiency by 2025

The Chinese government published its 2025 energy industrial efficiency improvement action plan in end-June. The plan aims to improve energy efficiency of energy-intensive industries such as steel, base metals, fertilisers and cement.

As part of the plan, the government is introducing market-based instruments to incentivise producers to improve energy efficiency. One example is the multi-step electricity pricing mechanism for energy intensive industries. This suggests producers will face higher electricity prices when their electricity consumption per unit of product is above the industrial standard. We expect that this type of policies will put upward pressure on costs and should result in production cuts at less efficient producers over the next three years.

Moreover, the government announced that the total energy consumption target will no longer be binding over the next three years, conditional on energy efficiency targets being achieved. This should reduce the trade-off between short-term economic development and industrial green transition.

The action plan restates the government’s target of reducing energy consumption per unit of GDP by 13.5% by 2025 compared with 2020. According to the government, this will be achieved by a lower share of heavy industries in the economy and energy efficiency improvements within the heavy industries over coming years.

We expect that China will achieve its industrial energy efficiency target by 2025 as it is not particularly ambitious. In December 2021, the Ministry of Industry and Information Technology announced that the 2025 energy intensity reduction goals would be 2% for steel, 3.7% for cement clinker and 5% for aluminum compared with 2020. These are realistic objectives and can be reached through energy saving retrofits in the plants instead of requiring fully industrial reform.

Steel hub Tangshan sets up hydrogen strategy to advance the green transition

Tangshan city government published its 2025 hydrogen development plan to stimulate the green transition of the traditional steel production hub in Northern China. The city-level development plan follows the guidelines set by the Chinese national hydrogen strategy from now to 2035. According to this, the use of hydrogen as an industrial by-product (i.e. from coke oven gas) is acceptable in the short term but a complete switch to green hydrogen in steel production should be considered the ultimate goal.

The Tangshan government plans to reach a hydrogen capacity of 60,000 t/y by 2025, of which 30,000 t/y will be green hydrogen and the rest is expected to come from coke oven gas. The total green hydrogen capacity target for China is 100,000–200,000 t/y by 2025, which means Tangshan will produce 15–30% of Chinese green hydrogen capacity by then. Tangshan’s share of national GDP is ~0.7%, while it is likely that its renewable capacity will be ~0.3% of total Chinese solar and wind capacity by 2025.

In the medium term, hydrogen direct reduction iron (DRI) is expected to contribute to the development of a hydrogen industry in Tangshan. Hebei Iron & Steel Group, a major steelmaker in Tangshan, announced in 2019 that it plans to construct a 1.2 Mt/y H2DRI plant by 2025. If solely reliant on hydrogen, the new capacity will consume ~60,000 t H2/y. The actual consumption will be lower because the plant is not expected to be fully reliant on hydrogen initially.

Tangshan also plans to have >3,000 fuel cell vehicles on the road by 2025, ~6% of the Chinese 2025 target, and >2,000 of them will be heavy-haul trucks. Assuming a mileage of 100–200 km/day for the hydrogen buses or trucks, as well as a hydrogen consumption of 8 kg/100 km for trucks and 5 kg/100 km for buses, these vehicles will consume 7,000–14,000 t/y of hydrogen by 2025.

Total investment in key projects should be ~$3 bn by 2025, 2–3% of annual local GDP. The hydrogen plan sets out investment in hydrogen generation with renewable power capacity, hydrogen refuelling stations, hydrogen trucks assembling, and fuel cell vehicle test and operation centre.

Despite the significant financial commitment required, the detailed development plan and the momentum of seeking green transition of the traditional steel production hub should make it more likely for the plan to be implemented, allowing Tangshan to achieve its hydrogen development goals.

Chinese SOEs issue green bonds to finance investment in low-emission technologies

Six Chinese state-owned enterprises (SOEs) issued corporate green bonds in June with two to three years maturity to finance investment in low emissions technology such as combined heat and power, and energy saving technologies in the steel, aluminium and chemical industries. The bond issuances generated between $30–150 M, with interest rates of 2.3–2.6%.

China issued $95 bn in green bonds in 2021, making it the second largest source of green bonds after the US. Proceeds from green bond issuance were earmarked for energy saving, pollution reduction, renewable power and energy storage projects. More than half was used to finance renewable power generation and UHV lines, while a quarter was used to finance green transportation, green buildings and pollution reduction projects. Around two thirds of this issuance met internationally recognised Climate Bonds green definitions.

The interest rates of the green bonds are lower than the 3.2–3.3% interest rate for non-green corporate bonds of similar maturity issued by other state-owned enterprises, and are also lower than the two-year green bond issued by private enterprises with a 5.5% interest rate. One reason for this, is that green bonds are more typically issued by SOEs with higher credit ratings. The lower funding cost should make it easier for them to advance green transition projects (which are mostly capital intensive) than for other businesses.

Find out more about our Sustainability Services.

Our reputation as an independent and impartial authority means you can rely on our data and insights to answer your big sustainability questions.

Tell me more