In the absence of global carbon pricing, the Carbon Border Adjustment Mechanism (CBAM) is a key policy to help the EU manage domestic decarbonisation goals within the globally traded commodities market. Yet the CBAM is a blunt tool. CRU finds that the CBAM would not equalise EU and non-EU carbon costs nor effectively discriminate between high and low carbon materials.

The EU’s Carbon Border Adjustment Mechanism is a key pillar of its Fit for 55 package

In its Fit for 55 package announced on 14 July 2021, the European Commission proposed the detailed legislative steps to be taken to achieve at least a 55% emission reduction by 2030 from 1990 levels, equivalent to a ~40% reduction from today. Alongside the revisions to the Emissions Trading Scheme (ETS), the Carbon Border Adjustment Mechanism (CBAM) is one of the key policies relevant for commodity markets.

What is the CBAM and why is the EU proposing it?

To meet its 2030 and 2050 emission reduction targets, the EU is increasingly pushing its domestic industry to decarbonise. Emission reduction efforts will have a knock-on effect on EU commodity production costs, as producers face climate policy-related cost inflation through exposure to increased carbon prices or, in some cases, the adoption of greener, but more expensive, technologies. This raises the risk of locking in the carbon leakage – where more expensive, lower carbon EU supply is displaced by cheaper, more carbon-intensive imports from jurisdictions with less ambitious climate targets – that is already apparent today under the current policy regime.

The EU has measures in place to tackle carbon leakage under the existing ETS rules: energy-intensive industries deemed at risk of carbon leakage only pay for a portion of the direct emissions that occur on site as they are given free emissions allowances. Some EU countries also pay compensation for emissions costs incurred through purchased electricity. However, these measures dampen the price signal needed to incentivise a shift to lower carbon manufacturing processes and have not been wholly effective at eliminating carbon leakage. As an alternative, the EU is now proposing the CBAM. Instead of compensating domestic producers for carbon costs, the EU is proposing to ‘level the playing field’ by charging for the carbon content of imported energy-intensive goods such as steel, aluminium and fertilizers. The CBAM will only be payable from 2026, though importers will need to report the emissions content of their imports from 2023–2025. The CBAM and ETS free allowances will run in parallel from 2026-2035, with ETS free allowances gradually phased out during this period as CBAM is ramped up. Full Scope 1 carbon costs will apply to all EU production and imports from 2035.

The table below shows the steel, aluminium and fertilizer products to be included in the CBAM scheme. CBAM is mostly confined to basic materials and their key intermediates. Value chain coverage is broadest in the steel sector, covering both raw materials (e.g. pig iron, DRI/HBI) and downstream fabricated products.

Proposed CBAM product coverage for the steel, aluminium and fertilizer sectors

| Sector | HS codes | Included | Key exceptions |

|---|---|---|---|

| Steel |

72 7301–7311 |

|

|

| Aluminium |

7601 7603 –7609 |

|

|

| Fertilizers |

2808 2814 283421 3102 3105 |

|

|

DATA: European Commission and CRU

How will different commodities be affected?

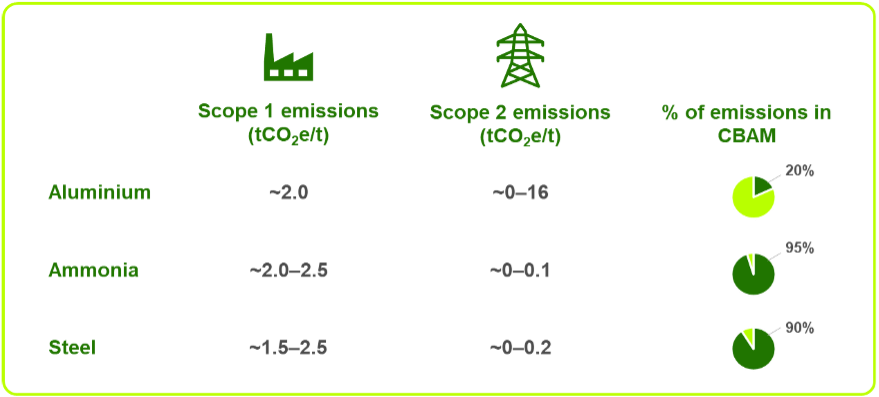

The exposure of individual commodities to the CBAM will depend on the carbon intensity of the product, the source of emissions, and prevailing commodity and carbon prices. The chart below details the typical carbon emissions intensity of aluminium, ammonia and steel production. Scope 1 emissions refer to direct emissions from company-owned and controlled resources. Scope 2 emissions refer to the embodied carbon in purchased electricity. Aluminium has the highest emissions intensity, with Scope 1+2 emissions of 2–18 tCO2e/t Al, of which Scope 1 emissions account for ~20% on average. Ammonia and steel have similar Scope 1+2 emissions of ~1.5–2.5 tCO2e/t, with Scope 1 emissions accounting for 90–95% of emissions.

Representative Scope 1 and Scope 2 emissions and CBAM coverage, tCOe/t product

DATA: CRU; NOTES: (1) steel emissions refer to BF-BOF, (2) For the purpose of this comparison, all aluminium and ammonia electricity is assumed to be purchased

DATA: CRU; NOTES: (1) steel emissions refer to BF-BOF, (2) For the purpose of this comparison, all aluminium and ammonia electricity is assumed to be purchased

Under current CBAM proposals, importers will only be charged for direct Scope 1 emissions. As mentioned above, the CBAM will initially be discounted to offset the free allowances given to EU producers under the ETS, meaning full Scope 1 emissions will not be charged until 2035. These design choices have several implications:

- CBAM will not equalise EU and non-EU carbon costs: the CBAM methodology is based on the average Scope 1 carbon costs that EU producers face across their whole production output. However, due to the ETS design, marginal EU output is exposed to full Scope 1 carbon costs. During the phase out of free allowances from 2026-2035, marginal EU production will face much higher carbon costs than the CBAM charged on imports. This has the effect of locking in carbon leakage for an extended period as marginal volumes produced with the EU will not be able to compete with imported material. A further insight specifically looking at this issue within the steel sector will be published in the coming weeks.

- Low-value commodities with a high proportion of Scope 1 emissions will feel CBAM effects more than high-value commodities: on a Scope 1 basis, aluminium, ammonia and steel all have similar emissions intensities, ~2.0 tCO2e/t. After adjusting for the free allowances given to EU producers, importers will initially only be charged for ~25% of Scope 1 emissions (i.e., ~0.5 tCO2e/t) in 2026, rising to c.2.0 tCO2e/t by 2035 when EU free allowances are removed. At current carbon prices, this implies a CBAM range of $30–120 /t. For high value commodities such as aluminium with typical prices >$2,000 /t, this cost increase can be easily absorbed by the market. For low value commodities such as ammonia, which typically trades at ~$400 /t, CBAM costs equate to cost inflation of 8–30%.

- CBAM will favour imports of electro-intensive commodities: the decision to restrict CBAM to Scope 1 emissions means aluminium imports, whose carbon footprint mostly comes from the electricity used in the electro-intensive smelting process, will not pay for the majority of their emissions. This will put them at an advantage to EU producers who have to pay electricity-related carbon costs.

- CBAM will not significantly differentiate between high and low carbon aluminium: given its high electro-intensity, the differentiation between lower and higher carbon aluminium is mostly determined by the source of power. Omitting Scope 2 emissions from CBAM means that producers using coal-based electricity will be charged the same CBAM levy as those using renewable electricity.

CBAM is just one driver of greater emissions disclosure

Despite the CBAM’s shortcomings, commodity exporters to the EU should take note. The current CBAM proposals are just the first iteration and the EU is looking to broaden the scope of emissions coverage to include more commodities, downstream products and other sources of emissions (e.g., Scope 2) in the future. Irrespective of the CBAM rules, commodity producers will increasingly need to declare the emissions footprint of their product, as stakeholders up and down the value chain call for greater emissions transparency as they seek to measure and reduce emissions from their supply chains.

To find out how CRU’s value chain emissions analysis tools can help you benchmark emissions performance or to learn more about the asset-level data and emissions curves readily available on CRU's new interactive web-based platform, click here.

To receive email alerts to all CRU Sustainability Insights, including the forthcoming analysis of CBAM on the competitiveness of the EU Steel sector, please register your details here.

Find out more about our Sustainability Services.

Our reputation as an independent and impartial authority means you can rely on our data and insights to answer your big sustainability questions.

Tell me more