The initial impact on commodity markets from EUs new Carbon Border Adjustment Mechanism will be limited

New EU legislation on emission reduction by 2030 sets a precedent for what policy might look like in the rest of the world. The new Carbon Border Adjustment Mechanism and tighter regulation around the EU Emissions Trading System are expected to have a limited initial impact on commodity markets, as policymakers opt for a slow phase-in from 2026. The design of the CBAM, and its omission of Scope 2 carbon emissions, means CRU expect the proposed measures to have a larger impact on the pricing of ammonia and steel, than on aluminium.

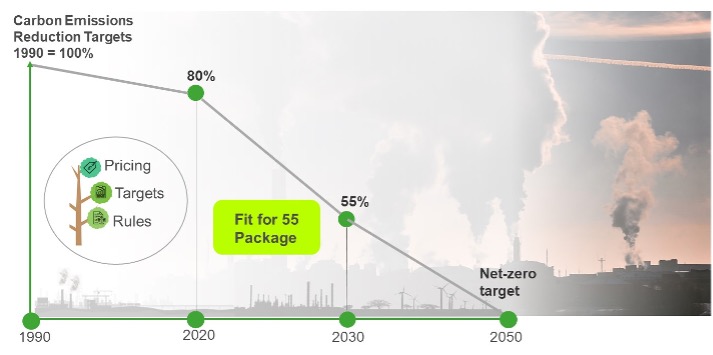

On 14 July 2021 the European Commission published its ‘Fit for 55’ package in which it proposes the detailed legislation required to achieve the continent’s climate ambitions under the European Green Deal.

A range of legislative streams from emissions trading to land use regulation

The European Green Deal sets out the European Commission’s vision for a climate-neutral continent by 2050 and is one of its six policy priorities for the 2019 to 2024 period. In its Fit for 55 package, the Commission proposes the detailed legislative steps to be taken to achieve the first milestone towards its 2050 net zero target: the net reduction of greenhouse emissions by at least 55% by 2030 from the 1990s level. This is a very ambitious target: between 1990 and 2020 carbon emissions in the European Union had declined by around 25%. The package covers all aspects of the EU’s climate-related policies and involves different legislative streams, including:

- Revision of the EU Emissions Trading System (ETS);

- Introduction of Carbon Border Adjustment Mechanism (CBAM);

- Revision of the Energy Tax Directive (ETD);

- Amendment to the Renewable Energy Directive (RED);

- Amendment of the Energy Efficiency Directive (EED);

- Reducing methane emissions in the energy sector; and

- Revision of the Regulation on the inclusion of greenhouse gas emissions and removals from land use, land use change and forestry.

The proposed package will now be scrutinised by the European Parliament and the European Council representing national governments, a legislative process that will go into 2022 and which will likely lead to changes and amendments.

The pace of cutting carbon emissions needs to increase to meet the new targets

DATA:European Comission and CRU

Why it matters: EU climate legislation will eventually lead to higher carbon costs for commodity producers at home and abroad

The revisions to the EU’s ETS – and closely related introduction of a CBAM – are of particular importance to the steel, aluminium, and fertilizer markets.

Under current ETS legislation, EU commodity producers are compensated for a large part of their carbon emissions (typically between 70% and 80%). The revised ETS will see compensation for so-called Scope 1 emissions - direct emissions from company-owned and controlled resources - phased out from 2026, with complete removal by 2035.

Compensation for Scope 2 (electricity-related) emissions will remain in place. Under the revised ETS regime, EU commodity producers that derive most of their emissions footprint from purchased electricity (e.g., aluminium, EAF steel) will see less cost inflation than those with mostly Scope 1 emissions (e.g., ammonia, BF-BOF steel).

From 2026, the EU will launch the CBAM and importers of steel, aluminium and fertilizers will have to report and pay for emissions embodied in their products. Importers will not have to pay for the full emissions content. To mirror the ETS changes, the CBAM will be confined to Scope 1 emissions and adjust for the free allowances given to EU producers. In other words, the full Scope 1 carbon costs will not be charged for until 2035. Given the slow phase-in of these measures it remains to be seen whether the 2030 emissions reduction target can be achieved.

Which commodities will be most affected by the CBAM?

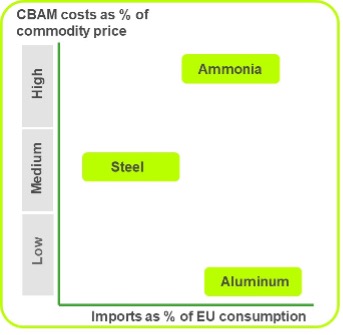

The extent to which the CBAM will impact commodity prices and trade flows will be driven by the relative cost of CBAM levies vs commodity prices, the ability of importers to source lower carbon material and the carbon intensity of the marginal supplier. On this basis, CBAM impacts will be highest for ammonia, medium for steel and lowest for aluminium. The aluminium industry will be least affected by the CBAM given the omission of Scope 2 emissions and higher commodity prices in this market. Ammonia is likely to see the highest cost inflation from CBAM, given its relatively low price and high proportion of Scope 1 emissions.

CBAM design means it will affect ammonia and steel more than aluminium

DATA: CRU

Over time, the CBAM and ETS revisions will put inflationary pressures on European commodity prices and reshape global trade flows.

The legislation has broader implications too. The European Union is one of the world’s most important regulatory bodies. With its Fit for 55 package the European Commission proposes concrete steps to reduce greenhouse gas emissions. Just like the EU’s taxonomy for sustainable activities, aimed at guiding the financial markets towards a low-carbon economy, it can be expected that the Fit for 55 package will become a benchmark for other countries to follow.

We expect that the Fit for 55 package will be the first of similar policy announcements over the coming years, with a number of countries already committing themselves to similar targets and measures ahead of COP26 in November. As a result, the commodities industry can expect to face higher carbon prices across the supply chain in much of the world as not only the EU but other countries to intensify their efforts to decarbonise their economies.

We will be examining the impacts of the Fit for 55 package in more detail over the coming weeks. Sign up to the new CRU Sustainability insights series to receive our analysis of what the revised ETS and new CBAM mean for the commodity markets.

To receive email alerts to all CRU Sustainability knowledge and insights.Please register your details.