The second phase of the EU Sustainable Financial Disclosure Regulation entered force in January 2023. To fight greenwashing and improve comparability across products, financial market participants and financial advisers are now required to publish Principal Adverse Impact assessments to show how their investment decisions and advice impact on the environment or human rights. The latest move in the EU is part of a wider trend globally to improve disclosure regulations, including on biodiversity. The capital-intensive commodity markets will need to adapt to tightening regulatory standards.

Latest EU sustainability reporting requirements force financial sector to act to avoid greenwashing accusations

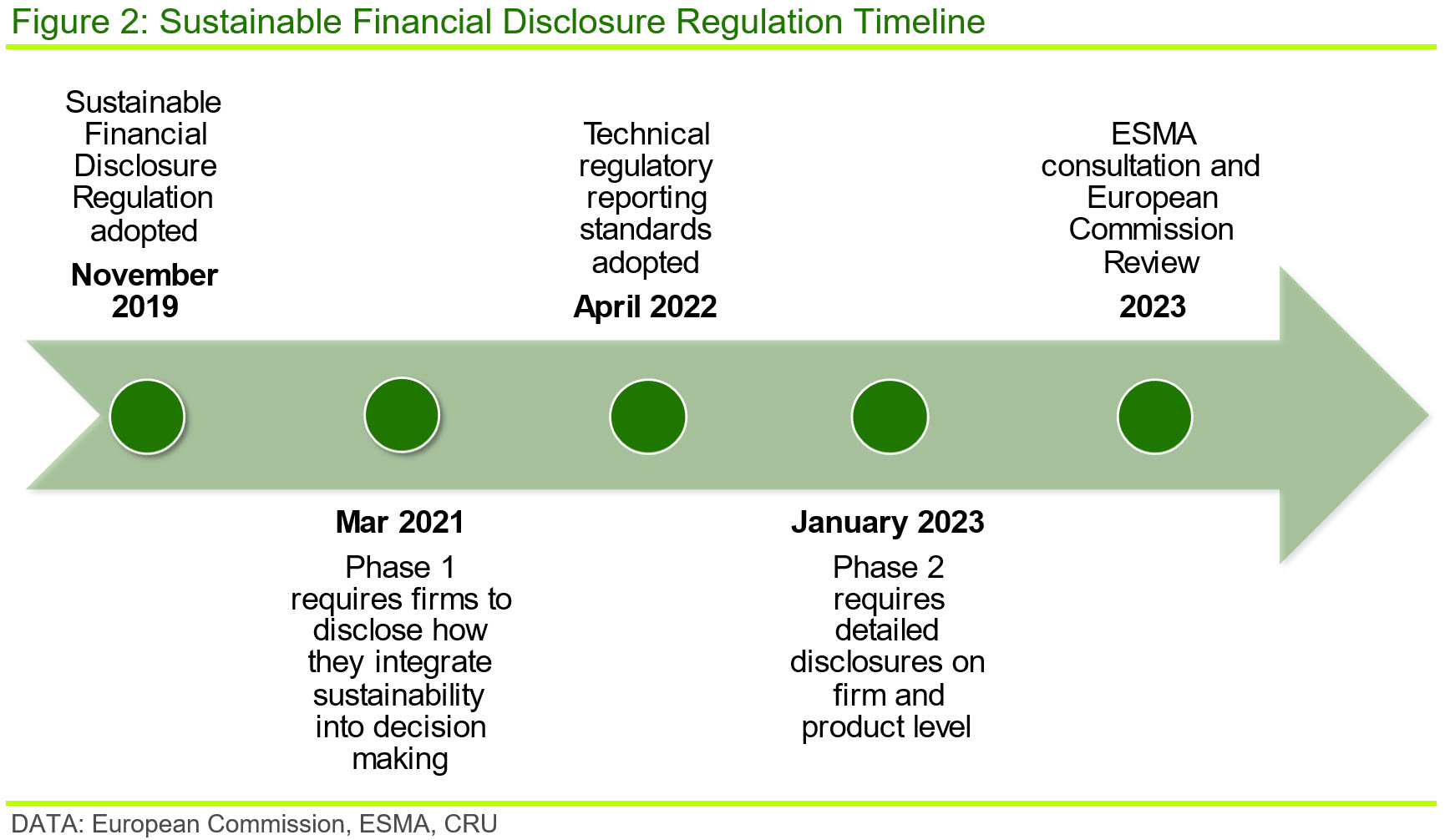

In early 2019 the EU adopted the Sustainable Financial Disclosure Regulation (SFDR), which has been applied since March 2021. The regulation sets out the disclosure regulations with respect to sustainability-related activities for financial market participants (e.g. asset managers and banks) and financial advisors.

The SFDR has been introduced gradually, with the first phase of disclosure requirements launched in March 2021. It requires asset managers and advisors to set out in broad terms how they integrate sustainability risks in their decision-making process or investment or insurance advice.

The second phase of disclosures was launched in January 2023 following the adoption of technical regulatory reporting standards for disclosing sustainability-related information in April 2022. Financial market participants and financial advisors are now required to publish Principal Adverse Impact (PAI) assessments in which they set out the adverse impact of any investment decision or advice on sustainability factors such as the environment, social concerns, human rights or anti-corruption. Disclosures must be provided on:

- an entity level by publishing an annual PAI statement on their website. This applies to financial market participants and financial advisors and covers the whole business on an aggregate level.

- a product level by publishing PAI information in pre-contractual financial product documentation, such as fund information. This requirement applies to financial market participants only.

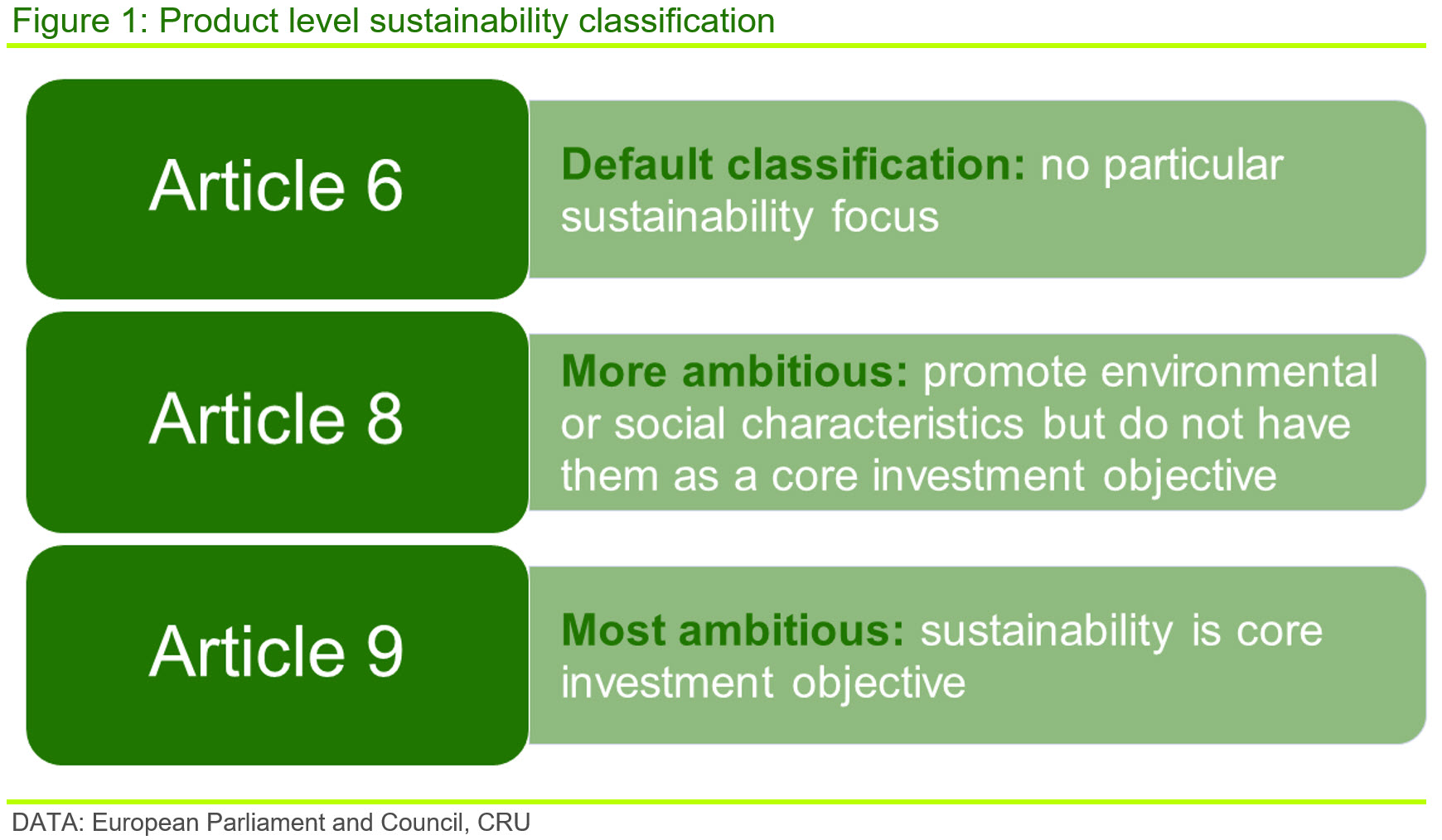

The technical standards aim to improve the quality and comparability of information provided by financial market participants about the sustainability performance of their financial products. Financial market participants must classify their products in three categories: Articles 6, 8 and 9.

The overarching aim is to combat ‘greenwashing’, i.e. making exaggerated claims regarding the environmental credentials of products and services. ‘Greenwashing’ has been identified as a major obstacle to the development of green financial products and consumer products as it could mislead investors and consumers. Over recent years, the global financial industry has been rocked by a number of high-profile greenwashing cases, with financial regulators investigating the conduct of a number of financial market participants. Up to now, accusations of ‘greenwashing’ could be reputationally damaging but faced no legal financial penalty.

The recent high-profile greenwashing cases and the launch of the second phase of SFDR in January 2023 had a significant impact on the labelling of financial products. Many asset managers, including some of the largest asset managers globally, reclassified their previously more ambitious Article 9 products as Article 8 products to reduce disclosure requirements and the reputational risk of potentially being accused of greenwashing.

Policymakers are addressing remaining issues and considering tougher sustainability rules

EU policymakers are now addressing remaining issues. One issue is the (mis)alignment of the SFDR’s technical regulatory reporting standards with the EU taxonomy for sustainable activities.

The EU’s taxonomy regulation entered force in July 2020 and establishes a list of environmentally sustainable economic activities. The taxonomy’s aim is to provide more certainty for investors, protect private investors from greenwashing, encourage businesses to become more climate-friendly and channel investments into these sustainable activities.

In early-2022, against strong opposition from a number of EU member states, the European Commission added specific economic activities involving nuclear and gas to the list of sustainable activities. In mid-February 2023, the EC published a new Delegated Regulation, which amends and updates the existing disclosure requirements of Article 8 and Article 9 with respect to fossil gas and nuclear energy activities to ensure alignment with the EU taxonomy for sustainable activities.

Correctly capturing environmental impacts in the Principal Adverse Impact Statements, which are required as part of the disclosures, is another issue. Currently financial market participants are allowed to use estimates to quantify the environmental impact of their investments when actual data are not available. This could be misleading, in particular with respect to Scope 3 emissions.

Policymakers are also concerned that the current classifications are not specific enough. To address this, the European Securities and Markets Authority (ESMA), the EU financial regulator, proposed the introduction of quantitative thresholds to make the distinction between Articles 6, 8 and 9 funds clearer. The EC will conduct its own review of the SFDR this year, with a final assessment likely to be published by early-2024.

Commodity markets will need to adapt to tougher sustainability disclosure regulations

Regardless of the finer details of any sustainability financial disclosure regulations, the fact that disclosure regulations are being tightened globally will have a profound impact on commodity markets.

In addition to the EU’s SFDR, policymakers globally are also in the process of implementing the recommendations of the Task Force on climate-related financial disclosures and are eagerly awaiting the recommendations of the Taskforce on nature-related financial disclosures. These are expected later this year. Moreover, the EU launched its Corporate Sustainability Reporting Directive in January 2023, which requires EU businesses and foreign businesses exporting to the EU to publish environmental and social information on their activities along the entire supply chain.

While ESG and sustainability investing faced headwinds in 2022, the drive to reach net zero and achieve wider sustainability objectives, including on biodiversity, will be one of the top priorities for investors over coming years.

For the capital-intensive commodities markets, financial market developments and regulation are particularly important as they can have a significant effect on shareholder value and the cost of capital. Corporates that fail to develop credible sustainability strategies, in particular relative to peers within the same industry, will increasingly risk being excluded from asset allocation decisions. The EU’s latest moves are also significant as they might be a precursor for policy and market developments elsewhere.

To discuss any of the issues covered in this or any of our previous Insights please reach out to CRU Sustainability.Find out more about our Sustainability Services.

Our reputation as an independent and impartial authority means you can rely on our data and insights to answer your big sustainability questions.

Tell me more