The Australian government plans to tighten the emissions ceilings imposed on large emitters in the industrial sector in an effort to align the emission targets with the nation’s updated climate goal for 2030. Although the reform will be built on the existing policy framework and policymakers have been careful to take the emitters’ readiness into account, large emitters are likely to face greater compliance challenges as emission targets are gradually raised over the next decade.

Australia to enhance emissions requirements for the industry

Elected in May 2022, the Australian government led by prime minister Anthony Albanese passed its Climate Change Bill in September 2022, raising the country’s climate ambition from a 26-28% reduction target under the previous government to now 43% reduction by 2030 compared with 2005 level.

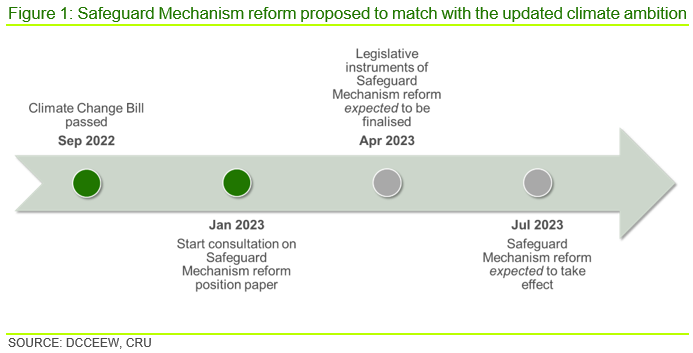

The Australian Department of Climate Change, Energy, the Environment and Water (DCCEEW) held a consultation between January and February 2023 on the proposed Safeguard Mechanism reform. The Safeguard Mechanism reform will be fundamental to meeting this more ambitious target and focuses on large emitters in the industrial sector, involving the power generation, mining, oil and gas extraction, manufacturing and waste sectors. The reform is one of a series of ongoing actions forming Australia’s climate change strategies including actions on renewable power, electric vehicles, technology, emissions monitoring and reporting, and international cooperation.

The government is expected to finalise the legislative instruments by April so that the reforms can take effect on 1 July 2023, the start of Australia’s 2023-24 fiscal year.

Emissions intensities to fall by 4.9% per year to align with national climate change goal

The Safeguard Mechanism was introduced by the previous Turnbull Coalition government and came into force in 2016. It was designed to curb emissions by large emitters with direct carbon emissions over 100,000 t CO2e per emitter per year, covering ~28% of current total emissions.

The current Safeguard Mechanism imposes an ex ante aggregate emissions ceiling (n.b. the ‘baseline’) for all emitters, but ex-post emissions cap adjustments are allowed per request in some special cases. This means that the current mechanism has a hard cap on total emissions in principle but not necessarily in practice.

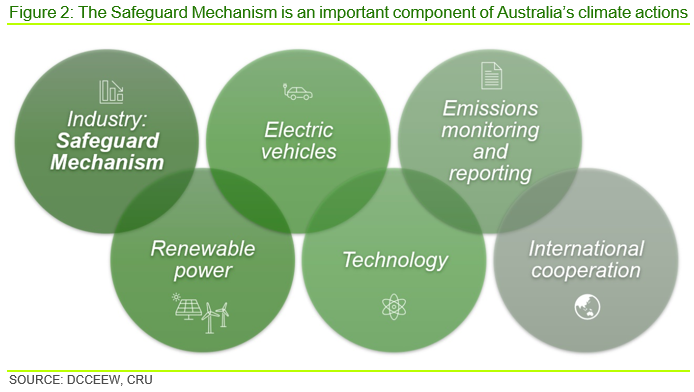

To achieve the country’s 2030 emissions target, the government now intends to set a clear and binding cap of aggregate emissions out to 2030. It proposes to set an upper limit of 99 Mt CO2-e for annual emissions of Safeguard facilities by 2030, falling gradually from the estimated 143 Mt CO2-e in 2022-23. This requires ~30% emissions reduction over the coming years.

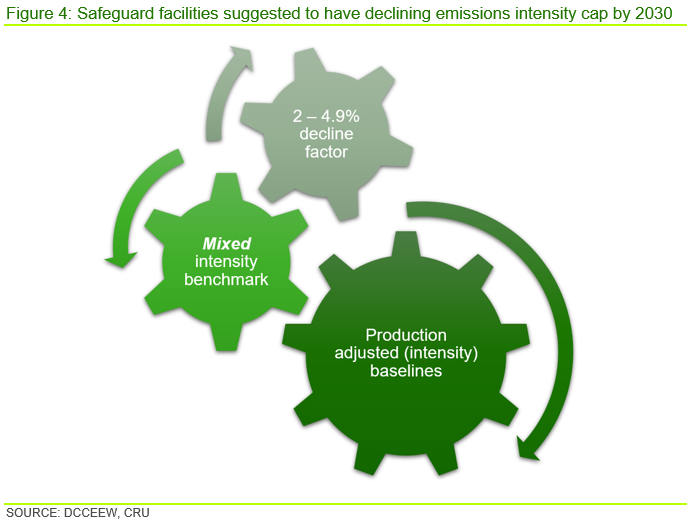

The government proposes to adopt production-adjusted baselines to all facilities to achieve the target, which means it plans to exert an emissions intensity cap for the industry.

The emissions intensity cap for each existing facility will be a weighted average of a site-specific baseline and an industry baseline by 2030, accounting for the facility’s readiness without compromising the overall target. In the near term, the government intends to put greater weight on the site-specific baseline but by 2030, all capacity in the same industry will be exposed to a uniform emissions intensity cap. In practice, the site-specific baselines will be set using the past four years’ data of the facility’s emissions-intensity values, reflecting each facility’s site-specific emissions level, while the industry average emissions intensity will be reviewed and finalised by the government. New facilities are proposed to be benchmarked to the international best practice to incentivise them to adopt the most efficient technology in carbon emissions mitigation.

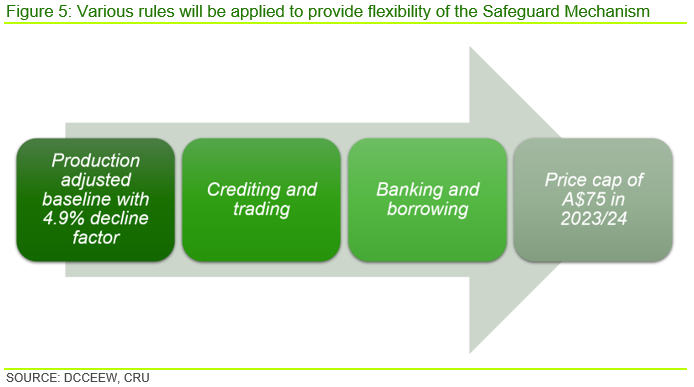

Moreover, the government proposes to reduce the baselines by 4.9% per year until 2030 on domestically-oriented industry, so that the emissions intensity cap will fall each year. The imposed reduction will be lower than 4.9% but no less than 2% per year for emissions-intensive trade-exposed (EITE) facilities to avoid carbon leakage.

Note that although 80% of the Safeguard participants are identified as EITE facilities according to the proposal – as long as their import and export value accounts for over 10% of domestic production value – only the facilities that exceed a certain cost impact threshold will be eligible for the preferential decline factor: a facility will only be eligible if it needs to spend over 3% of its revenue to meet its compliance obligation based on the unadjusted baseline.

This suggests that the facilities that are most advanced in emissions control and overperform their emissions targets are less likely to benefit from a preferential decline factor in the coming years, even if they are exposed to carbon leakage risks. Instead, it would be the companies with higher emissions intensity and higher compliance burden that would benefit from a less ambitious emissions reduction target to avoid carbon leakage.

EITE to receive additional assistance, including a fund

Apart from the preferential decline rate, EITE industries are expected to benefit from a dedicated fund of A$600 M ($400 M) from the A$1.9 bn ($1.3 bn) Powering the Regions Fund (PRF). The government is establishing the PRF with the aim of accelerating the emissions reduction transition, focusing on decarbonising existing industries, developing new clean energy industries, workforce development and purchasing carbon units. The facilities will also have preferential treatment for access to other PRF streams.

In the recent consultation exercise, the Australian government also acknowledged the industry’s interest in an Australian version of a cross border adjustment mechanism (CBAM) and announced to undertake a review without committing to this policy at this stage. The EU reached a provisional agreement on a CBAM in early-January.

Tradable credits to facilitate lowest cost net-zero transition

To facilitate the net-zero transition at the lowest possible economic cost, the government proposes to introduce a crediting and trading scheme that would allow emitters that exceed their emission targets to sell their unused credits to those emitters that fail to meet their specific targets.

Moreover, to promote price stability, banking and borrowing of the credits are allowed in the proposal, including full banking to 2030 and borrowing up to 10% of the baseline each year. The government proposes to charge an interest rate of 10% on all borrowings to recognise the benefit of early abatement through disincentivising delaying abatement.

Carbon price to be capped at $75 /t for 2023-24

To control the upside risk of rapidly increasing carbon prices faced by the companies, the government proposes an A$75 /t CO2-e ($52 /t CO2-e) price cap for financial year 2023-24, with further annual price increases to be set at consumer price inflation plus two per cent. The current ACCU price is less than half of the proposed cap.

The government lifted the penalty to deter non-compliance and expects it will be effective (n.b. the penalty on non-compliance will be set at A$273 /t CO2-e ($188 /t CO2-e)). It does not plan to collect any penalty revenue from the Safeguard Mechanism and expects the Safeguard Mechanism obligations to be met.

2026 review to ensure hitting the 2030 target

The government intends to review the effectiveness of the proposed reforms in 2026-27 to ensure that the 2030 emission reduction target will be met. The government might make adjustments to the decline factors, the regulations on flexibility arrangements and the cost containment measure for 2028-29 onwards.

Impact varies and low-emission products to be favoured

The tighter emission cap of the Safeguard Mechanism will raise the overall cost of the affected sectors and reduce the demand from end users, which tends to have downward pressure on industrial output. Facilities with lower emissions intensity than industry average can be shielded from the negative impact to some extent because they can make a profit from the extra credit earned. This means that there will be winners and losers within the industry despite the overall contractive impact on industrial output in the short term.

In the long term, the tighter cap of the Safeguard Mechanism and rising carbon prices should incentive investment in low carbon technology and accelerate Australia’s decarbonisation efforts. This could have spillover effects on Australia’s major trade partners such as China, Japan, Korea and the USA, especially if Australia decides to follow the EU by introducing a carbon border adjustment mechanism aimed at providing a level playing field for domestic producers and importers.

Find out more about our Sustainability Services.

Our reputation as an independent and impartial authority means you can rely on our data and insights to answer your big sustainability questions.

Tell me more